Can Trump’s plan actually make housing affordable again? In today’s post, we’re diving into two of Trump’s core housing promises and exploring whether economists think his plans are realistic. Then, I’ll share some data that no one else is talking about that might just prove them all wrong.

After the November election, the National Association of Realtors released their predictions of how a Trump’s housing plan could impact the housing market. They’re not optimistic. Let’s look at some of the ideas Trump floated at a speech at the Economic Club of New York on September 5th, 2024.

Trump’s Housing Plan #1: Cut regulations

Trump said: “We will eliminate regulations that drive up housing costs with the goal of cutting the cost of a new home in half. We think we can do that. The regulations alone …cost 30% of a new home. . .”

NAR responded to this saying: “…those figures appear to be dramatically overblown. The National Association of Home Builders, a longstanding industry critic of regulations, estimates that site work and related permit fees account for 7.4% of the average new-home cost, with overhead and general expenses accounting for an additional 5.1%.”

So NAR is saying that the regulatory costs of building a home are only 12.5%, not 30%. This got me curious because I had recently read a report from the National Association of Home Builders that said the regulatory costs make up 24% of the sale price of the home. So I did a little digging to figure out which, if any, numbers are correct.

How much do regulations cost home builders?

In the NAR article there is a link to a report so I was able to see the line items they were referring to. I really appreciate when people link their sources.

The line items they were referencing were building permit fees, impact fees and water and sewer fees. What the report did not include was Land Development Regulations: these are costs related to zoning, land use approvals, and environmental regulations. They usually come into play earlier in the process before home construction starts.

The report NAR was referencing was only looking at the costs within an individual build, not for developing a whole community. It also didn’t include Building Codes Compliance, which are Expenses for adhering to evolving building codes and standards. This might include requirements to use more energy efficient materials or fire rated materials in a build, adding to the cost of a home.

The report also didn’t include Delays and Holding Costs: These are Financial impacts resulting from prolonged approval processes and compliance requirements. If the builder or developer is paying interest on a loan while the community is in development, the delays while waiting for approvals will cost them additional interest payments and those amounts can be substantial, especially in a higher interest rate environment.

I was talking to a friend just yesterday who had a client who was supposed to close on their new construction home in June and didn’t end up closing until December due to permitting delays. That’s a lot of interest expenses for something that isn’t built.

So it appears that a number closer to 24% is more likely realistic than the 12% stated by NAR.

How did Trump Get His Number?

But where did Trump get 30%?

I kept digging and found that, the national multifamily housing council has said that government regulations make up 40% of a multifamily build. I don’t know for sure, but I would guess that the 30% number is an estimate of the combination of single family and multifamily regulation costs.

And if you think I’m playing soft ball with Trump, just hang on a minute. I’ll get to some crazy things he has said. But in this case, I think his numbers were reasonable.

The real question is, will Trump be able to limit these costs? Trump’s plan for housing deregulation might be enticing, but it’s important to keep in mind that many of these regulations are at the state and city levels.

Part of Trump’s campaign was that the Federal government is going to stay out of local government decisions. Also, even if he could cut regulatory costs in half, so just for argument’s sake, he makes them 15% of the total build, that isn’t going to get housing costs lowered by 50%.

However, he didn’t say that reducing regulations alone would bring the cost of new construction down 50%. Much of the cost of a new home build is in materials, from lumber to drywall, from piping and electrical, and all of that has to be shipped. Bringing down the cost of shipping and manufacturing could really help with the cost of new home builds. We’ll see if he can do that.

But, he has some other goals as well.

Trump’s Housing Plan #2: Pressure the Fed to Lower Interest Rates

The next real estate issue mentioned by NAR that may be impacted by a Trump presidency is pressure to lower the interest rates.

Trump says: “Reducing mortgage rates is a big factor. We’re going to get them back down to, we think, 3%, maybe even lower than that, saving the average homebuyer thousands of dollars per year.”

Lending Tree’s senior economist, Jacob Channel, says, “The president doesn’t set mortgage rates….Trump probably wouldn’t be able to arbitrarily decide to lower them even if he wanted to.”

Trump could eventually nominate a new Federal Reserve Chairman, but even that wouldn’t guarantee anything.

But there’s more to it.

What Channel says is true, HOWEVER, rates set by the Fed are influenced by the greater economy.

High rates happen when there is inflation and the fed raises rates to slow down the spiraling of prices. That’s exactly what has happened with today’s higher rates. If Trump can have an impact on the economy, then we may see rates come down.

Daryl Fairweather, the chief economist at Redfin, believes that economic work has already been done. She told MarketWatch. “mortgage rates will likely be lower next year — not because of the president, but because inflation is pretty much under control now.”

So maybe this part of Trump’s plan for revitalizing the housing market has already been accomplished, though not by Trump. But can he really get mortgage rates as low as he claims?

What Economists are not talking about

There are a couple of things that concern me about what all these people are saying will happen with rates.

Let me show you something. I want you to look at these graphs the way I am looking at them. Now, I am not an economist, but when I’m looking at the data, something doesn’t sit right with me. The story that we are hearing on the news doesn’t match the graph that I am seeing on my screen.

I want you to tell me if you see the same thing I am seeing. Let me show you.

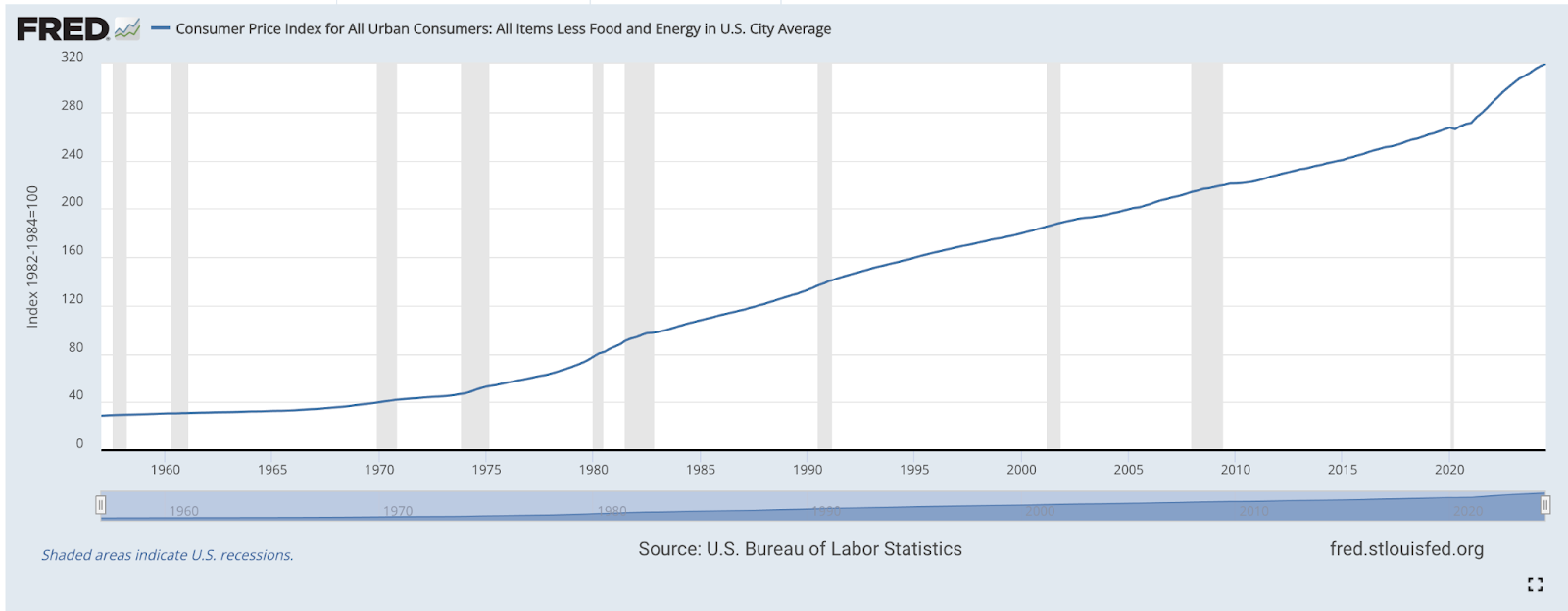

Changes in the Consumer Price Index

This is the Consumer Price index from about 1970 on. You can see how it has a fairly steady gradual slope of increasing prices from 1974 to 2020. There are two significant bumps. In the 1980s and again over the last four years.

Both of these times involve a historic period of inflation, followed by a presidential election.

I don’t think we can make a straight connection between what happened in the 1980s and today. Just because there was inflation and a presidential election, that doesn’t mean the scenario was exactly the same.

The 1970s and 80s were so incredibly different from today, so I just want to focus on the relationship between rising prices and interest rates. Because there is something to learn here that applies to 2025’s real estate market.

Follow me for a minute while we walk through this.

The Price of Goods and Mortgage Rates in the 1970’s and 1980’s

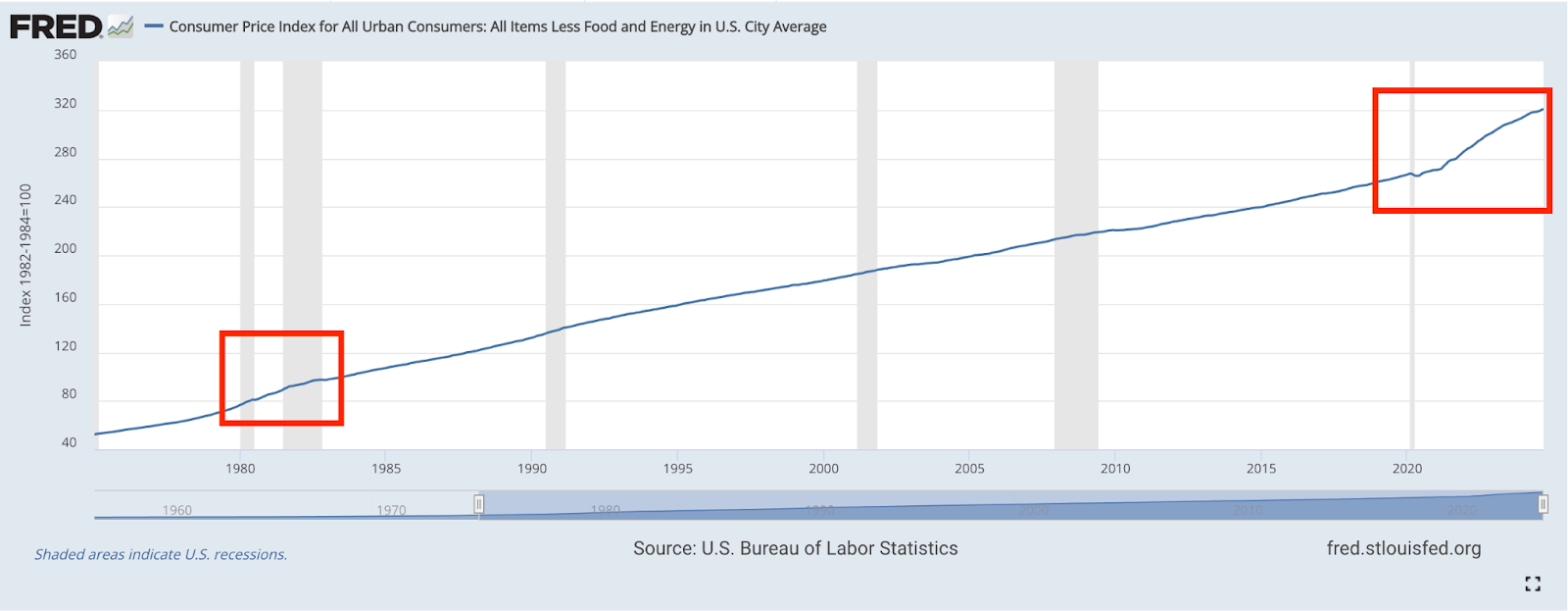

In 1979, prices of goods and services started to rise. And they continued to rise until about February of 1983-84 when they started to stabilize and return to the same trajectory they were on before. Remember that date because we’re going to circle back to it in a minute.

In 1978, you can see that mortgage rates started to rise. This was before we can actually see the prices rise on the graph. Rates then reached a peak of 16% in April 1980. Reagan took office in January 1981, rates jumped again peaking to around 18% in October of 1981, before finally coming down to the baseline in his third year of presidency.

This is a great example of how economies aren’t quick things to move.

The CPI and Rates in the 2020’s

Now let’s look at 2020. You can see the drop in consumer prices right after covid hits. It was a massive price decline, or deflation, in like a week. And then what we think of as the Covid inflationary period started.

They told us at the time it was transitory inflation, meaning it’s related to a specific event and will go away quickly. But that isn’t what happened.

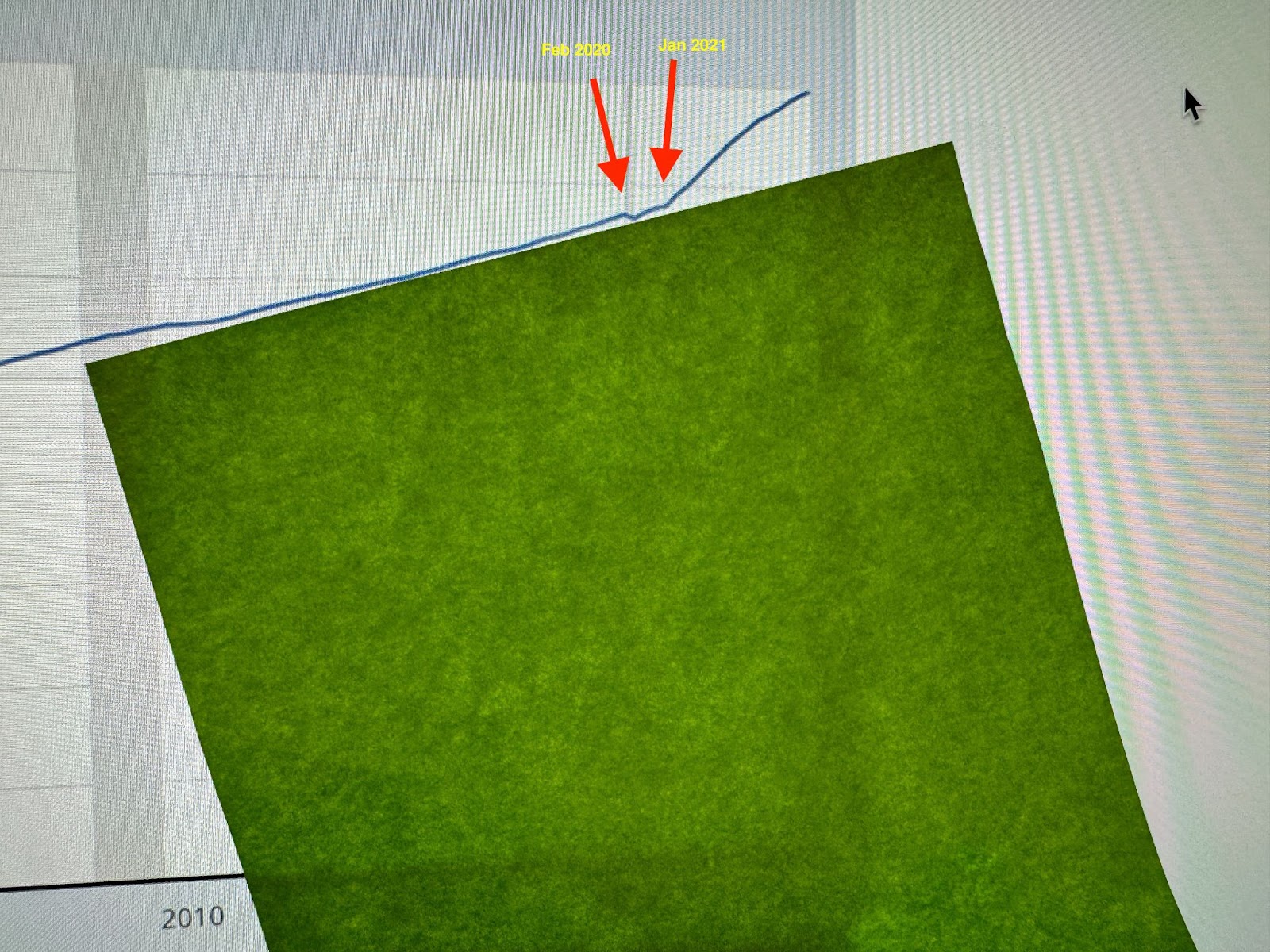

Now I want you to look a little closer at this graph. Look where the Covid deflation happens. And now look at the angle of the line for the first year after Covid hit. This is 2020. Does it look to you like the line is at about the same angle as the previous years, up until about February of 2021.

You can see this if you hold a straight edge up to the screen like this.

After the drop in 2020 the line is roughly the same angle until February of 2021. There is a slight increase in the angle, but it’s really February of 2021 that inflation starts to take off. And it keeps on with that upward trajectory at that new steeper angle pretty much until today.

I have a theory for why this happened.

Also, there is a little blip at the end of the graph where it starts to flatten a bit again. I think this is significant and we will talk about it in a minute as well, but first let’s look at the mortgage numbers during this second period.

Mortgage Rates and Inflation after Covid

Trump’s plan for housing requires lower mortgage rates, and that requires inflation to come down. But, there is this idea that inflation came from Covid. However, if we look closely at this graph I think it came from something else. And knowing what that is can help us understand what is going to happen next.

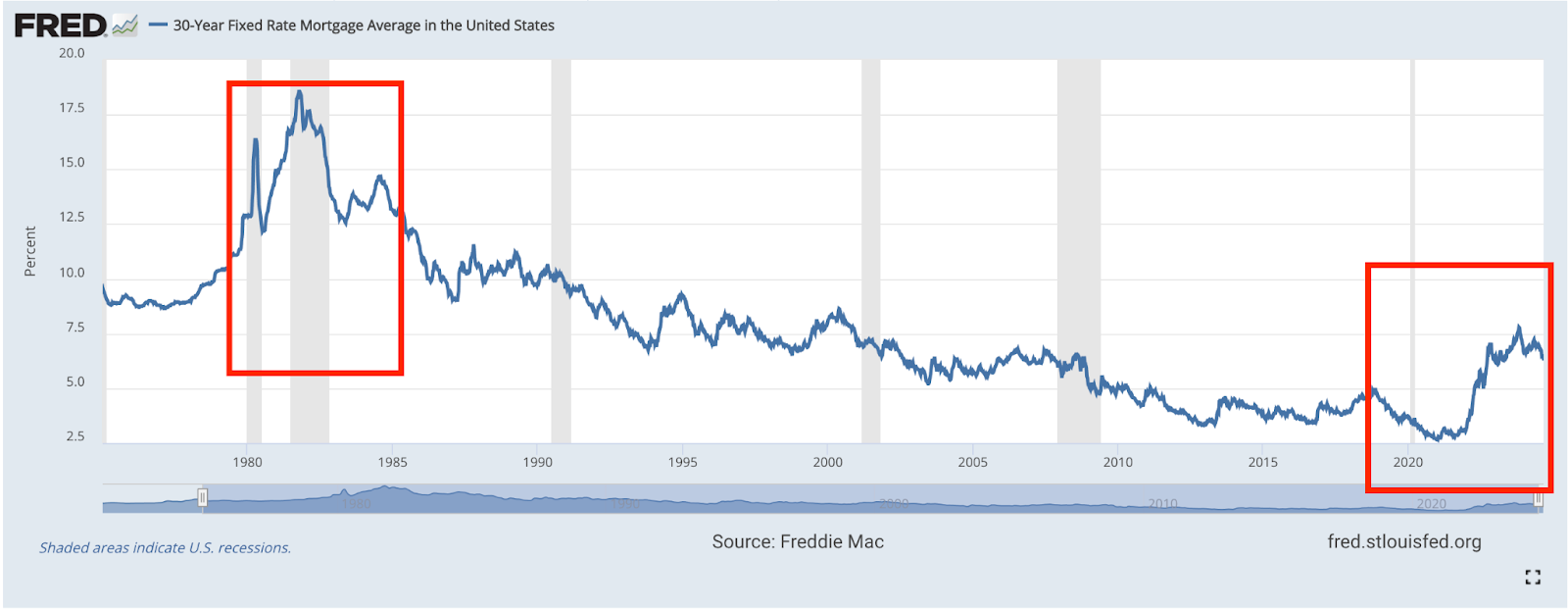

Mortgage rates after 2020 did the exact opposite of what happened in 1980. Instead of rates jumping, they dropped.

They were about 3.5% in February of 2020. By September of 2020, they were into the 2% range. And they stayed in that 2% range until January of 2022. Personally, I think this was a HUGE mistake of the Federal Reserve. And I personally don’t think either President was responsible for this rate drop.

I think the Federal reserve was trying to stimulate the economy because their fears of deflation were higher than their fears of inflation.

If you look closely at the graph, during the calendar year of 2020, there was no inflation. In fact, prices were lower than they were the year before. They were concerned that because of Covid, nobody would be buying anything because everyone was on lockdown. So they stimulated the economy with these rate drops to make businesses take risks.

Businesses started producing goods at great prices because rates were so low and Americans started shopping. At historic levels. Like, how many new TV’s were bought during Covid?

The Federal Reserve Created the Housing Price Spike

The Federal Reserve literally caused the mess we are in right now. If they had done nothing, maybe the economy would have tanked rather than getting so overheated that it caused the mess we have today. If they had dropped rates for 3 months and then brought them up maybe it would have been better?

Nobody really knows what would have happened if they had made different decisions. But I feel like we’ve forgotten the real story and it’s coloring what people say needs to happen.

At any rate, I truly think intentions were good here but the results were that housing prices got out of control. The other thing I know is that I would hate to be the person who has to make these decisions. They’re not easy decisions to make. But there’s more to the story.

Energy Costs and Not Enough Workers

Once the low rates got the inflation ball running, two things kept it spiraling.

The National Bureau of Economic Research did a study in 2023 and found that “the main contributors to the headline inflation shocks were energy prices (2.7 percentage points) and a backlog of work (1.7 percentage points).” By backlog of work, they mean too many job openings and not enough people to fill them.

But I think point number two, the backlog of work, again, cycles back to the Federal Reserve’s low interest rates. When rates are low, businesses hire new employees and expand on their products and services. This is what caused the backlog of work. So we’re really looking at two key points. 1) The Fed setting the rates too low and 2) energy prices being too high.

Trump’s plans for Housing Rates is Not Realistic.

2% is way too low for mortgage rates. That’s what got us into this mess of unaffordable housing.

When he talks about getting rates below 3% again, it is my hope that Trump is not really talking about mortgage rates but about the Federal Funds rate.

The Federal Reserve sets the Federal Funds rate. Again, this is not controlled by the President. The Federal Funds rate is the base rate that mortgage lenders use to set mortgage rates. Mortgage rates are usually a couple of points or so higher than the Federal Funds rate.

If Trump is saying that consumers will pay 2% that just isn’t realistic because it will again lead to the kind of inflation that we saw post Covid. If he is saying that the federal funds rate will be at 2% and mortgage rates will be 4-5%, that seems to me to be a more realistic benchmark to shoot for.

Whether he can accomplish this I think will depend a lot on the next point, energy. Another short history lesson and then I’ll tell you how all this ties back to housing.

The Impact of High Energy Costs

In 1973, countries in the middle east imposed an oil embargo. They stopped selling oil to the US because we were backing Israel during a war. This caused long gas lines, and prices of all goods and services tied to shipping started to spike.

In response to that, the US created the Strategic Petroleum Reserve.

Initially we purchased oil for the SPR stores from international sources, but eventually we started producing our own. The US has some of the most plentiful oil reserves in the world.

Incidentally, countries like Saudi Arabia, Qatar, and even Norway use their oil reserves as a way to fund government programs for their citizens rather than relying solely on taxes.

By the 1980s we had built up to a level of 500 million barrels. Reserve levels have gone up and down over the years, as we’ve fought different wars and released oil to provide that stability when the world gets unstable. This is what it is designed to do. But you have to keep restocking the reserve.

Restocking the Strategic Petroleum Reserves

By 2010, we had 726 million barrels and today, we have 387 million barrels. This is because we dipped into our reserves to stabilize gas prices and because the war in Ukraine exacerbated global supply of oil. Again, we’re supposed to do this, but you also have to restock it.

The last time it was this low was in 1984, when we first started growing our reserves. Notice this was also when inflation numbers finally started to decrease. When Covid hit in February of 2020, we had 634 million barrels in reserve. We are not currently restocking our supply to effectively prevent these fluctuations in energy costs.

There is a direct connection between the level of these oil stores and prices of goods and services in the United States because when levels are high, we are protected from potential supply disruptions, especially during times of conflict in the middle east, where a lot of oil comes from.

This is why the national bureau of economic research said that energy prices were primarily responsible for inflation over the last few years.

Trump’s overall economic plan certainly highlights the importance of domestic energy production. So maybe part of Trump’s plan for reducing housing costs comes from his proposed push for domestic production?

But what does that have to do with mortgage rates?

A lot…

If we can stabilize oil prices, by filling our oil reserves, prices for goods will stabilize. And if prices for goods stabilize, interest rates can come down. If interest rates come down, mortgages rates will come down. And if mortgage rates come down, housing will be more affordable.

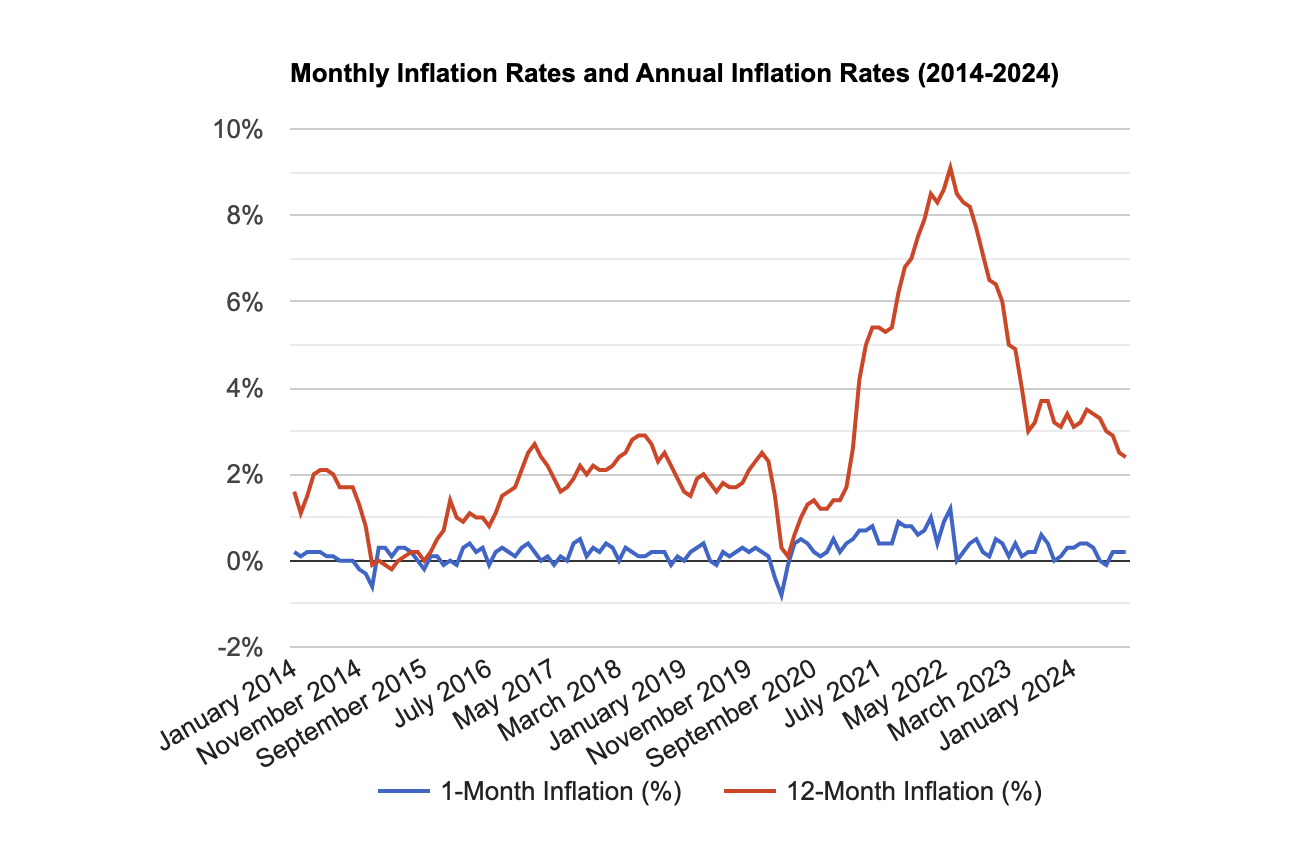

Inflation is Down, but not Prices

But we still need to talk about the blip at the end of the inflation graph. We’ve been told that the inflation numbers are no longer rising. And that is true. You can see that the angle of the line turns back almost, but not quite, to the more level angle that it was pre-Covid.

Here’s a chart of monthly and annual inflation rates for the last ten years. Yes, the rate at which prices are going up is declining.

The problem is, prices are still high.

They haven’t come down and wages haven’t kept up.

And since rates have been so high, while we’re not in a recession, the economy is stagnating and there isn’t a lot of competition for jobs.

When borrowing rates are high, companies don’t take on new employees to expand into new products and services and so there isn’t an economic push for wages to rise. So again, while there isn’t technically a recession, that doesn’t mean that people aren’t feeling the crunch of high prices and a less robust economy. In order to fix this, we fix the major things that play on each other for a strong economy. We need strong oil reserves, we need lower interest rates but not too low and we need one more thing that nobody is really talking about.

Trump’s Housing Plan doesn’t address part of the Housing Supply and Demand Problem

Regardless of what he does or doesn’t do, we still have some problems that won’t be an easy fix. Let’s give Trump the benefit of the doubt. Let’s say that interest rates come down, that builder’s permitting and compliance costs come down, and that inflation level’s out.

We still don’t have a good skilled labor force for construction to build more homes.

One of the drivers of higher home prices is simple supply and demand. Everyone agrees that the US Market is short on housing. Part of reducing housing costs is increasing the supply, and that takes skilled laborers. We don’t have enough of them. And simply trying to entice laborers from outside the US won’t necessarily fix that problem.

According to a study from UC Berkley, many immigrants arrive in the US with limited construction experience and knowledge of US safety practices. This is partly attributed to cultural differences and varying safety standards in their home countries. Many immigrants also enter the workforce as unskilled or semi-skilled laborers, concentrated in low-wage trades.

This suggests a lack of specialized training in specific construction skills.

Regardless of what happens with immigration policy, the US needs a strong trades educational program in order to build the housing supply we need. This won’t be quick or easy to implement. And I don’t see politicians talking about this problem.

I want to hear your thoughts about this because this should be the start of a conversation.